Japan’s return on equity (ROE) has undergone a measurable structural improvement over the past decade. This Japan ROE regime shift reflects convergence toward developed-market profitability levels that is not the result of a cyclical rebound or temporary fiscal stimulus. Rather, the available evidence indicates that the dominant driver has been sustained improvement in operating profitability, with capital returns and balance-sheet optimization playing a reinforcing — but secondary — role.

Chief Investment Officer

Distinguishing between these drivers is essential. An ROE expansion driven primarily by leverage or equity shrinkage tends to be finite and cyclical. An expansion driven by improved margins and capital discipline suggests structural change.

The data support the latter interpretation.

ROE Convergence in Context

Research Analyst

Market-implied aggregate ROE — derived from valuation ratios across broad Japanese equity indices — shows a sustained upward trajectory across multiple economic regimes: post-global financial crisis restructuring, Abenomics-era reforms, the pandemic cycle, and the current post-deflation environment.

The persistence of improvement across cycles is inconsistent with a purely macro-driven surge. It points to a change in corporate behavior and profitability dynamics underlying the Japan ROE regime shift.

To assess whether this shift is operational or financial, a DuPont-style decomposition provides clarity.

ROE = Margin × Asset Turnover × Leverage

Aggregate corporate data show that operating margins increased materially over the past 15 years, asset turnover declined modestly, and financial leverage fell rather than rose.

In other words, the improvement in ROE did not come from increased leverage. It came from higher profitability. Importantly, aggregate net assets expanded during this period, indicating that equity was not being broadly compressed in a manner consistent with purely denominator-driven ROE expansion.

The conclusion is straightforward: Japan’s ROE shift has been primarily numerator-driven.

Capital Returns and Balance-Sheet Optimization

Shareholder distributions have increased meaningfully in recent years. Buybacks reached record levels, and dividend payout ratios rose. At the same time, the long-standing system of cross-shareholdings continued to unwind, freeing capital and increasing transparency.

These developments mechanically support ROE by improving capital efficiency and reducing excess equity. However, the aggregate evidence suggests they acted as accelerants rather than as the core engine of the improvement.

A denominator-dominant ROE story would typically exhibit stagnant margins, rising leverage, and shrinking aggregate equity. Japan instead demonstrates rising margins, declining leverage, and expanding retained earnings.

Financial engineering contributed, but it did not define the regime shift.

Governance Reform as the Structural Catalyst

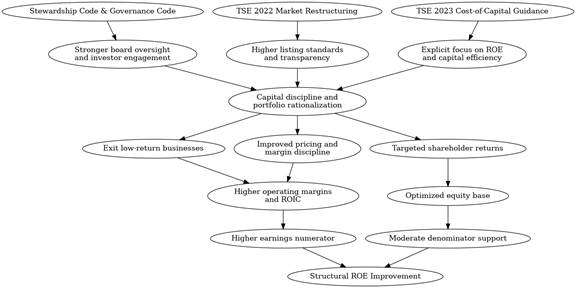

The transformation in profitability aligns closely with a decade-long evolution in Japan’s corporate governance framework. The introduction of the Stewardship Code and Corporate Governance Code, subsequent revisions strengthening board independence, the Tokyo Stock Exchange’s 2022 market restructuring, and the 2023 guidance emphasizing management accountability relative to cost of capital collectively altered managerial incentives.

Public disclosure requirements and segment restructuring created reputational and capital-market consequences for underperforming firms. Companies trading persistently below book value were explicitly encouraged to articulate capital efficiency strategies. This increased transparency and comparability across firms.

This “scoreboard effect” is a structural transmission channel: it pushes management to improve ROE primarily by strengthening earnings power and return on invested capital, and only secondarily through balance-sheet optimization.

The mechanism can be illustrated as follows:

The key observation is that the primary pathway flows through operating improvement before capital distribution effects reinforce the outcome.

The Macro Environment: From Deflation Constraint to Pricing Flexibility

For decades, persistent deflation constrained Japanese firms’ pricing power and reinforced conservative balance-sheet management. The recent emergence of sustained wage growth and moderate inflation represents a meaningful shift in the nominal backdrop.

The restoration of pricing flexibility allows revenue growth to translate into margin expansion rather than merely offsetting cost pressures. This macro normalization supports the governance-driven profitability improvements rather than replacing them.

The interaction between structural reform and nominal growth provides a more durable foundation for earnings power than either factor alone.

Implications

The evidence indicates that the Japan ROE regime shift is fundamentally rooted in improved operating profitability. Governance reform and enhanced capital allocation discipline changed managerial behavior. Capital returns and cross-shareholding unwinds reinforced the effect but did not create it.

This distinction matters for allocation decisions. Profit-driven ROE expansion reflects structural improvement in corporate economics. Such shifts tend to be more persistent and support sustained valuation re-rating, particularly when supported by institutional reform.

Japan’s convergence toward developed-market profitability levels remains incomplete. However, the direction of change is anchored in operating fundamentals rather than temporary financial adjustments.

The central question is no longer whether Japan’s ROE has improved. It is whether the profitability discipline now embedded in corporate governance can sustain the trajectory across sectors and cycles.

Structural profitability shifts rarely occur in isolation—they reflect deeper changes in governance, incentives, and capital discipline. Tiempo Capital evaluates international equity exposures, including Japan, within a broader investment management framework that emphasizes operating fundamentals, valuation discipline, and portfolio diversification. Learn more about our approach and contact us to discuss how global structural shifts fit within your long-term allocation strategy.

This material is for informational purposes only and does not constitute financial, legal, tax, or investment advice. All opinions, analyses, or strategies discussed are general in nature and may not be appropriate for all individuals or situations. Readers are encouraged to consult their own advisors regarding their specific circumstances. Investments involve risk, including the potential loss of principal, and past performance is not indicative of future results.